Featured

Selling a condo in Toronto can be challenging, especially when market conditions are uncertain. However, with the right strategy and execution, it’s possible to achieve strong results and help clients move forward with their next chapter.

This case study highlights the successful sale of a condo located at 6 Lakeshore Boulevard West in the iconic Tip Top Lofts building in downtown Toronto.

Selling a condo in Toronto can be challenging, especially when market conditions are uncertain. However, with the right strategy and execution, it’s possible to achieve strong results and help clients move forward with their next chapter.

This case study highlights the successful sale of a condo located at 6 Lakeshore Boulevard West in the iconic Tip Top Lofts building in downtown Toronto.

Selling a condo in Toronto can be challenging, especially when market conditions are uncertain. However, with the right strategy and execution, it’s possible to achieve strong results and help clients move forward with their next chapter.

This case study highlights the successful sale of a condo located at 6 Lakeshore Boulevard West in the iconic Tip Top Lofts building in downtown Toronto.

One of the most common questions I get is:

“Should I buy a condo or a freehold?”

The honest answer is: it depends on what you’re optimizing for.

And here’s the part most people miss: many buyers optimize for the wrong thing (usually “what feels like the best deal today”) instead of what matters over the next 3, 5, or 10 years.

This guide will help you decide quickly — and avoid the common mistake of buying the wrong type of property for your timeline.

A portfolio is intentional. It has a purpose, a time horizon, and risk controls.

In Toronto and across the Greater Toronto Area, “Spring Market” has a reputation: more buyers, more action, and (sometimes) better results.

But here’s the truth most sellers don’t hear often enough:

Spring is not automatically better.

It’s just different.

Most real estate “truths” are only true in one specific market cycle. The Toronto/GTA has a new personality every 6–12 months….so let’s clear it up. Below are 5 real estate myths I hear every week, and the actual variables that drive price, timing, and leverage in today’s market — without the fluff.

Based on the 2026 market outlook we’ve been discussing, the market likely won’t move in a straight line — and condos in particular may feel more pressure in the first half of the year, with improving conditions later as demand strengthens and new supply slows. The smartest sellers in 2026 won’t “wait and see.” They’ll plan around the market’s rhythm and control what they can control.

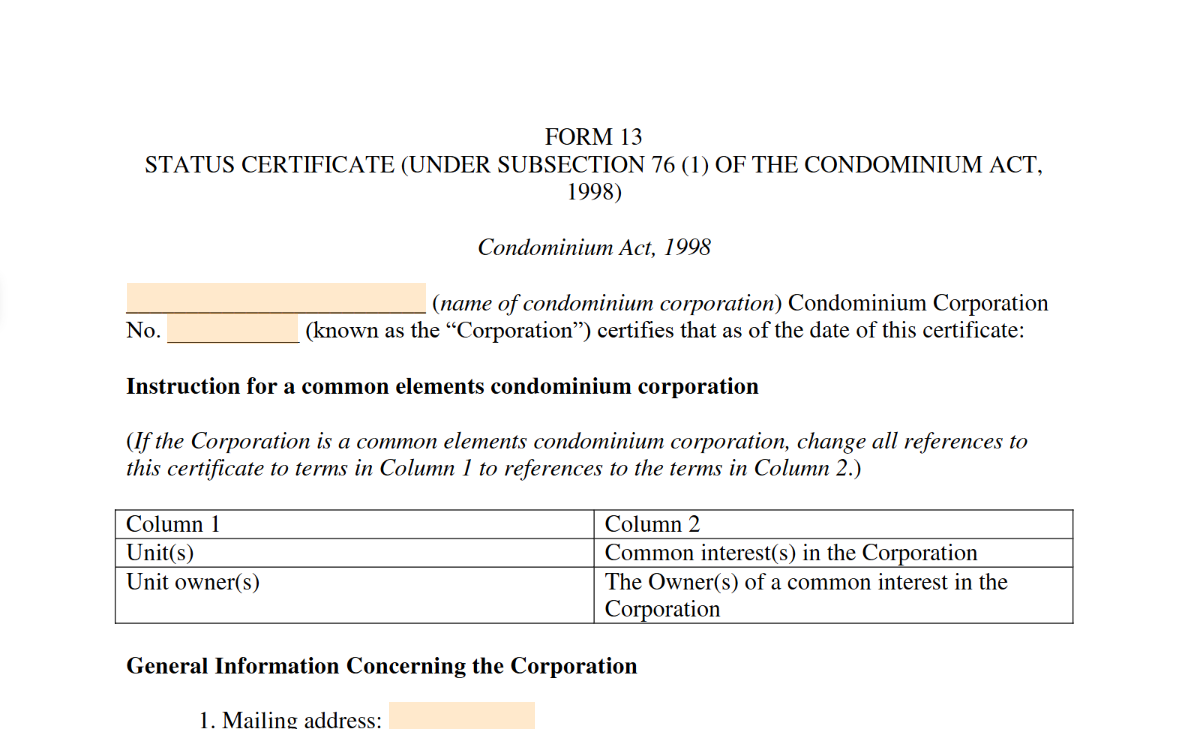

Condo listings are built to show you the highlights: the view, the kitchen, the amenities, the lifestyle. But if you’re buying a condo in Ontario, Alberta or any other province, the Status Certificate is the document that tells you what you’re really buying.

January is when we all pretend we’re becoming brand-new people. New calendar. New goals. Maybe even a gym membership that feels very real until February.

But if you want a financial reset that actually makes a difference (and takes less time than meal-prepping), pull up your most recent mortgage statement.